The Sun Has Won Research Note: Historical and Planned U.S. Electricity Generation

The Sun Has Won Research Note: Historical and Planned U.S. Electricity Generation

Rob Carlson, PhD

Managing Director, Planetary Technologies, LLC

Summary: Wind and solar now constitute the vast majority of newly constructed electricity supply in the U.S., reaching 99.7% of new net generation commissioned in Q1 of 2024. Fossil-fueled electricity generation, produced by burning coal or natural gas, peaked in 2007 and has since fallen by 14% through 2023. In contrast, over that same period, electricity production from renewables, here defined as the combination of wind and solar, has grown by 600 GWh, to about 20% of total U.S. electricity supply. The growth in renewables has more than made up for the decline of fossil fuels, and fossil fuels are now being displaced by the combination of wind and solar, facilitated by battery storage. Utilities and power planet operators expect to shut down increasing amounts of coal-fired electricity production. Some state markets are further into the energy transition than others. The combination of solar and batteries reduced natural gas usage during afternoon and evening hours in California in H1 2024 by approximately 50% compared with the same period in 2023. Similar impacts on gas use are emerging in Texas this year with the commissioning of new battery capacity. Widely trumpeted plans for significant new domestic gas-fired electricity generation are not yet evident in surveys of developers and utilities by the U.S. Energy Information Agency (EIA). While much is made today of a projected increase in electricity demand from data centers, which may delay the expected shutdown of some fossil-fueled production, the low price and capital efficiency of renewables will increasingly outcompete fossil fuels to meet that demand; the medium-, and long-term prospects for fossil-fueled electricity production in the U.S. are poor.

…

The mix of electricity production sources in the U.S. from 2001 through 2024 is shown in Figure 1. The electricity produced from fossil fuels, a combination of coal and gas, peaked in 2007 at 2.9 TWh and declined through 2023, falling by approximately 14%, to 2.5 TWh. Despite the large rise in natural gas used to produce electricity from 2007 through 2023, which is itself displacing coal-fired generation, the electricity produced from fossil fuel combustion declined even with an increase in total electricity production. The absolute contribution from nuclear and hydroelectric remained flat from 2001 through 2024. In contrast, the combination of wind and solar is growing, constituting >99% of newly commissioned supply in the U.S. in Q1 of 2024. Wind and solar together now supply the marginal watt in the U.S. The combination of wind and solar eclipsed the contribution of nuclear power to electricity production for the first time in March, 2024. Wind and solar together produced more energy than coal through July, an advantage that I expect to be maintained through the end of the year.

In 2024, warmer than expected temperatures across the U.S. increased the demand for cooling, and thus for electricity, which was supplied by increased renewable output and a slight increase in fossil-fuel combustion. From 2025 onward, the EIA expects renewable sources, in particular PV, to grow fast enough to continue supplying the marginal watt and also begin reducing gas-fueled electricity production.

…

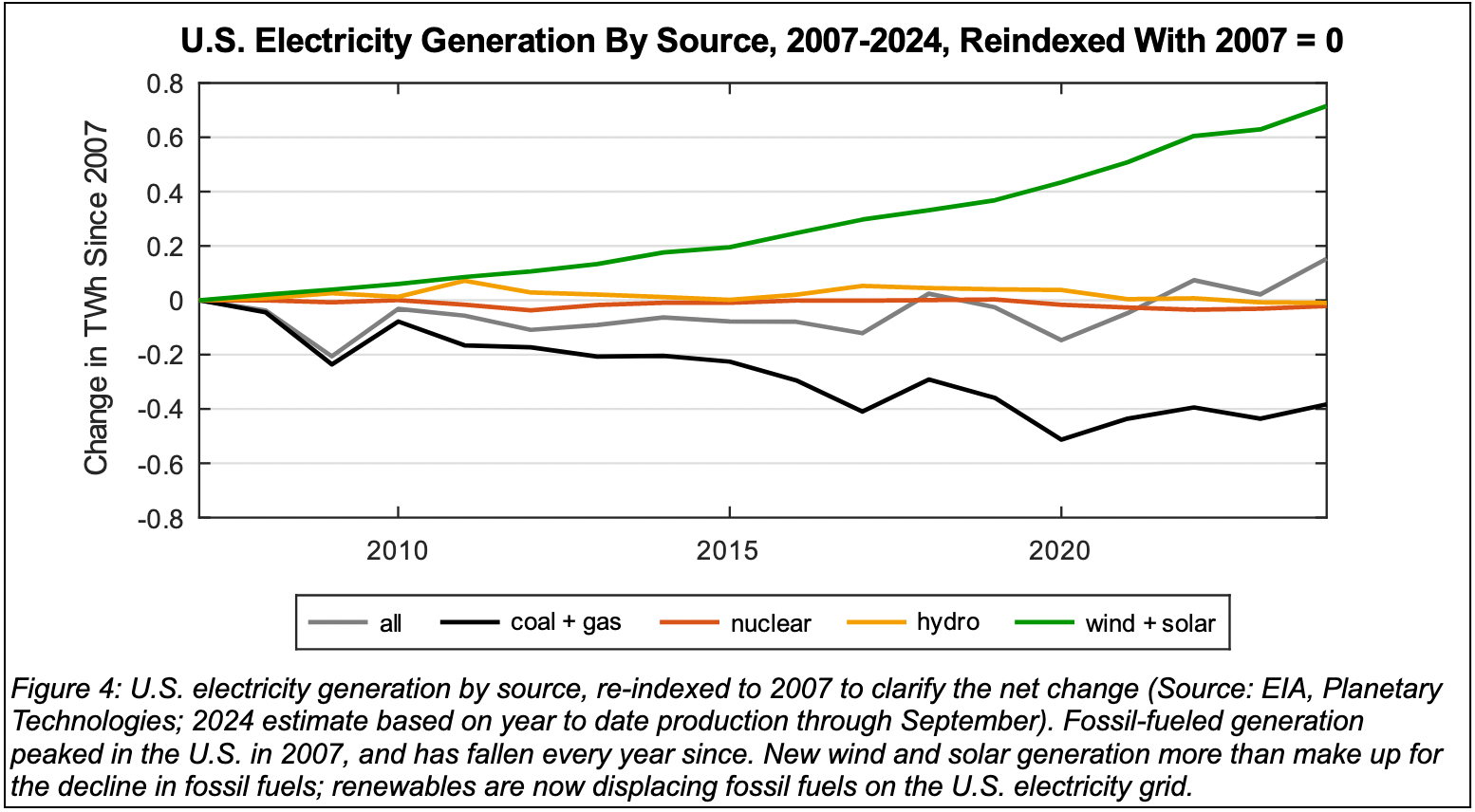

Peaking has peaked

The recent shift in the U.S. electricity supply mix, and in particular the change in fossil fuel combustion and renewable generation, is more obvious when the data in Figure 4 is re-indexed to 2007, as in Figure . Renewables have grown more than fossil fuels have declined, which, in the context of an increase in demand, meansrenewables have been providing all marginal growth while also displacing fossil fuels. Much is made today of an expected increase in electricity demand due to the growth of data centers. This demand may delay the shutdown of some fossil-fueled production. Yet renewables increasingly outcompete all fossil fuels in terms of energy efficiency and capital efficiency, and thus are the best investment for meeting new demand.

The cost of energy in the U.S. depends on the region in which it is generated and the region in which it is used. However, across the U.S., the maximum unsubsidized Levelized Cost of Energy (LCOE) for PV is now generally well below the minimum LCOE for natural gas turbines used for peaking, and in manycases is below the minimum LCOE for gas combined-cycle generation. The EIA forecasts that very few gas-fueled facilities that might come online by 2028 will produce electricity at a lower cost than PV. As one indication of the impact of this price differential on the development of new gas resources, industrial customers who plan to purchase electricity over decades will take these forecasts into considering when signing contracts, and are likely to specify that they are supplied from the lowest cost generation source. Beyond simple economic considerations, in California, CAISO, the operator of the California electrical grid, is implementing is implementing a policy preference to use renewables and batteries rather than fossil fuels; even with higher capex, the unsubsidized LCOE for the combination of PV and batteries is 1) approaching the lower end of the LCOE distribution for natural gas peakers, and 2) due to falling costs will soon encroach on the LCOE range for combined cycle generation. Gas-fired generation costs less than coal-fired generation, and PV-plus-batteries increasingly costs less than gas. The medium- and long-term prospects for coal- and gas-fueled electricity generation in the U.S. are poor, and that future is visible in planned new fossil generation capacity.

…

While just over 5 GW of new gas-fueled capacity was brought online across the U.S. during Q1 2023, only 67 MW of new gas capacity was commissioned during Q1 2024, a 98.7% drop. For context, there was about 510 GW of gas-fired generation capacity in the U.S. at the end of 2023, so achieving even 1% growth in gas-fired capacity would require a net change of about 5 GW. According to the EIA, in 2024 developers expect to add a total of just 3.2 GW of new gas combustion capacity, compared to at least 44 GW of wind and solar and at least 14 GW of batteries. However, as of September, approximately 3 GW of gas-fired capacity had already been reported retired in 2024, with a total of about 3.8 GW expected retirements by the end of the year based on EIA survey responses. Thus the net change for gas-fired capacity in 2024 is likely to be negative. To be clear, the total electricity generated from gas rose slightly in 2024 due to higher output from existing facilities, while, according to EIA data, the number and power output capacity of those facilities contracted. Additionally, about 2.6 GW of coal-fired generation will be retired in 2024, with none added. As a result, 2024 may be the first year in which renewables displace both gas and coal capacity from the U.S.grid. But one datum does not a trend make. Whether this turn of events is maintained over the short term will depend significantly on the rate of retirements and will have to be assessed on an annual basis.

Both gas- and coal-fired generation capacity are likely to shrink this year. Thus 2024 may be the first year in which renewables displace both gas and coal capacity from the U.S. grid.

Going forward, based on surveys of plant operators and utilities, the EIA does not expect more than modest new gas resources to be commissioned over the next five years (Figure 5), which of course will be offset by annual retirements. Instead, batteries are providing grid services formerly purchased from gas-powered generators. Net energy generation from solar grew 25% year on year through May, 2024. The EIA forecasts that net generation from solar will increase 42% in H2 2024 compared to 2023, and generation from wind will increase by 6%. Where there are already significant battery resources deployed in combination with renewables, gas use appears to be falling.